While the heaviest concentrations of capital continue to optimize and compete within the established corridors of Bali, a different class of investor is looking eastward. The narrative that Lombok and the Gili Islands are merely "the Bali of twenty years ago" is a marketing cliché that fails to capture the current commercial reality. In 2026, these are not purely speculative frontiers; they are active, high-performing yield engines operating with their own distinct logistical rules and demographic demands.

The data clearly indicates that the ceiling for performance across the Lombok Strait has risen dramatically. We are no longer looking at backpacker economies. We are analyzing sophisticated micro-markets that are currently matching the baseline occupancy rates of prime Seminyak and Canggu, albeit with different entry costs, operational hassle, and architectural requirements.

For the yield-focused investor, the question is no longer whether to cross the Wallace Line, but how to deploy capital effectively once there. Understanding the architectural sizing, budget tiering, and intense seasonality of these two distinct regions is the only way to ensure an asset converts potential into actual revenue.

The Macro Picture

Before drilling into the micro-dynamics of bed sizing and budget tiers, we must establish the baseline performance of both regions. The overarching data reveals a surprising parity in baseline demand, though the revenue generated from that demand differs significantly based on location and logistics.

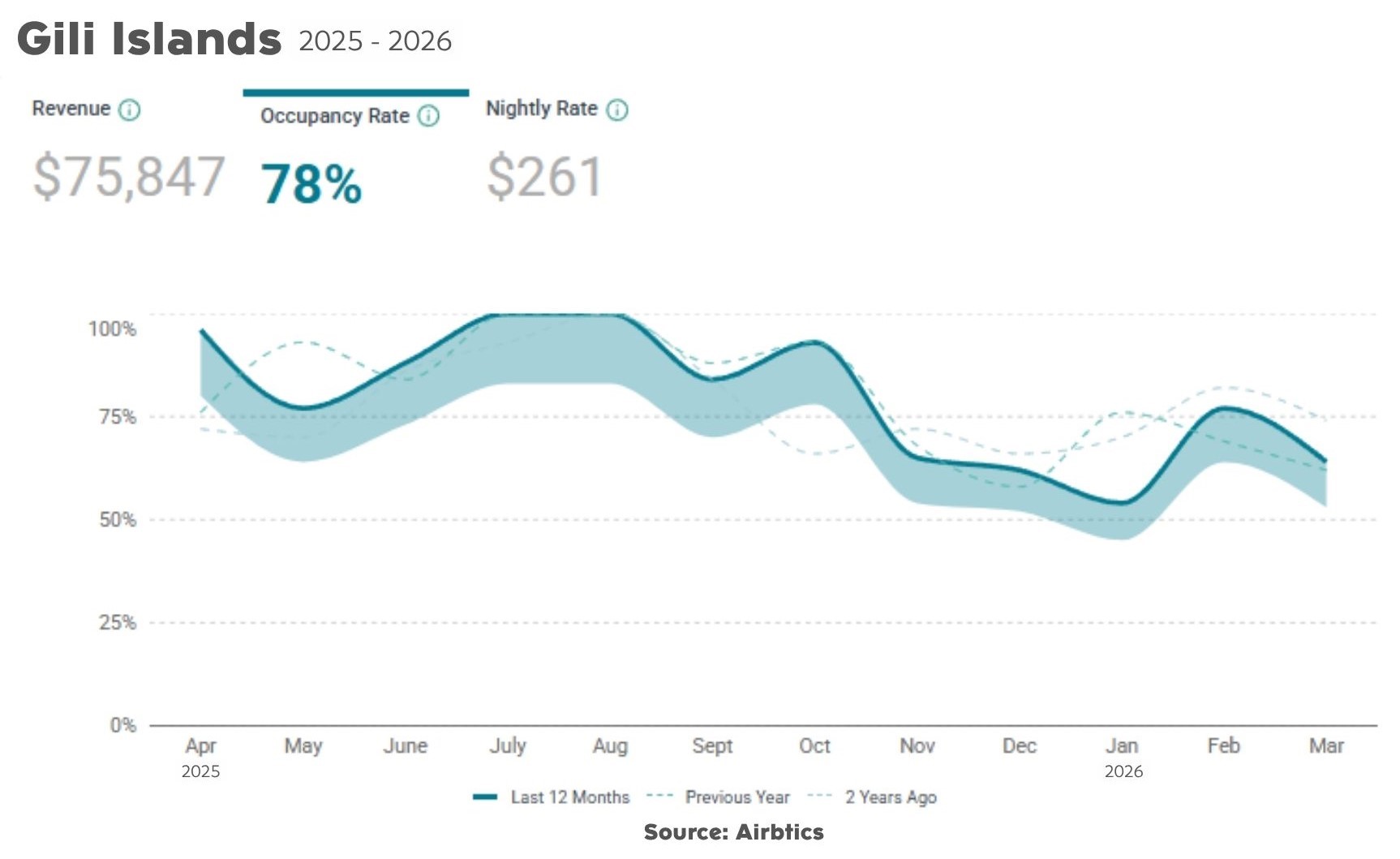

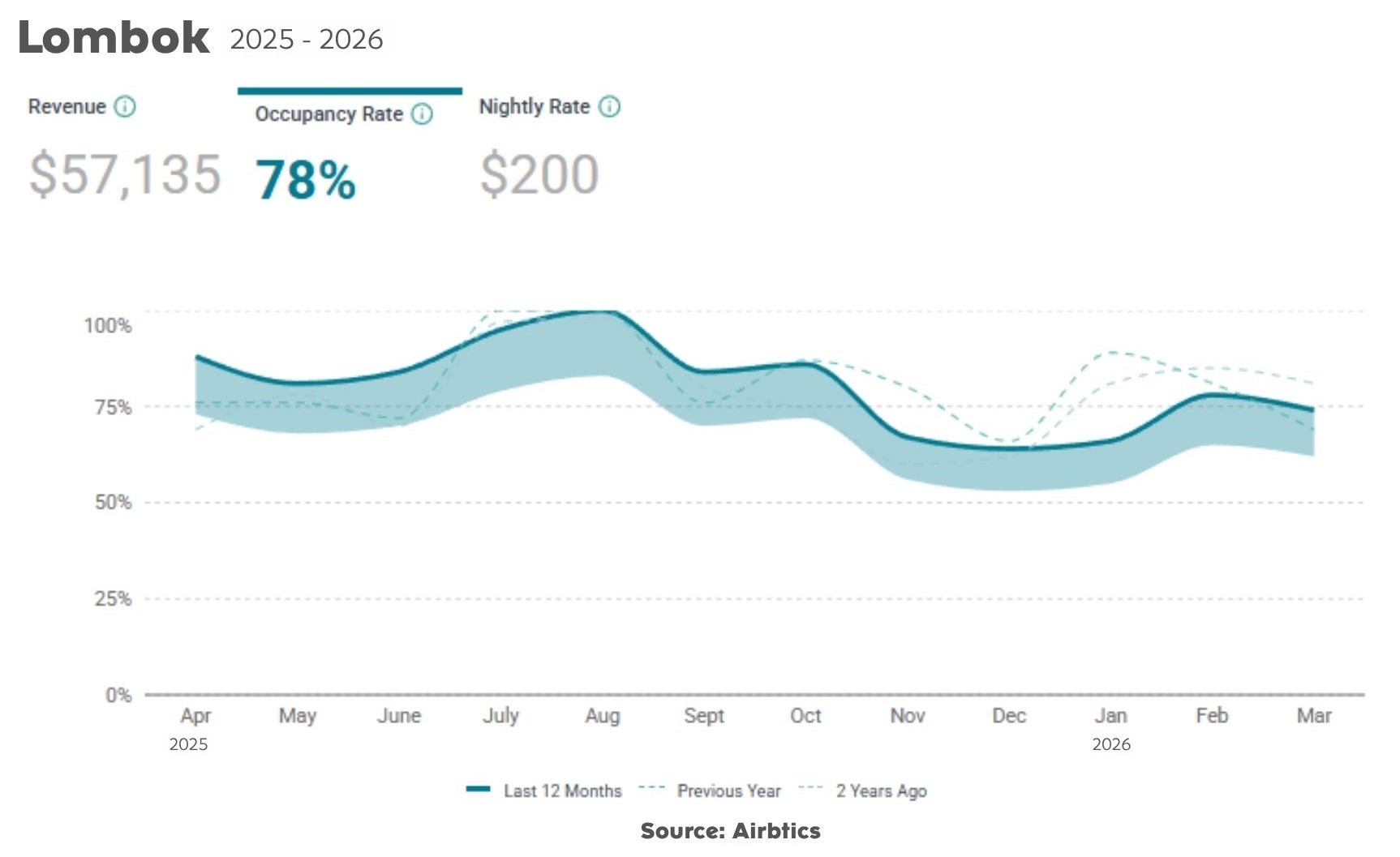

Looking at the trailing 12-month metrics, both the Gili Islands and Lombok are operating at a highly impressive 78% average occupancy rate. To put this into perspective, this is the exact same occupancy band currently sustained by the premium beachside zones of Seminyak and the residential corridors of Canggu.

However, the financial output of that 78% occupancy highlights the distinct nature of the two markets:

-

The Gili Islands command a significantly higher Average Daily Rate (ADR) of $261 (IDR 3,915,000), resulting in an annual revenue average of $75,847 (IDR 1,137,705,000). This high yield reflects the "island penalty" that guests are willing to pay for a localized, car-free, highly curated tropical experience.

-

Lombok, encompassing the Mandalika and Kuta regions, maintains an ADR of $200 (IDR 3,000,000), pulling in an annual revenue of $57,135 (IDR 857,025,000). While the top-line revenue is lower, this is offset by mainland advantages: easier access to construction materials, lower operational friction, and direct proximity to an international airport.

Both markets are highly viable, but they require entirely different product offerings to capture the top tier of their respective demographics.

Lombok as the Rise of the Mid-Sized Asset

Lombok is a market heavily defined by the surf, wellness, and emerging digital nomad communities. It attracts couples, solo professionals, and small groups who want the mainland infrastructure of Bali without the heavy urbanization. Capital deployed here must be engineered to match this specific demographic.

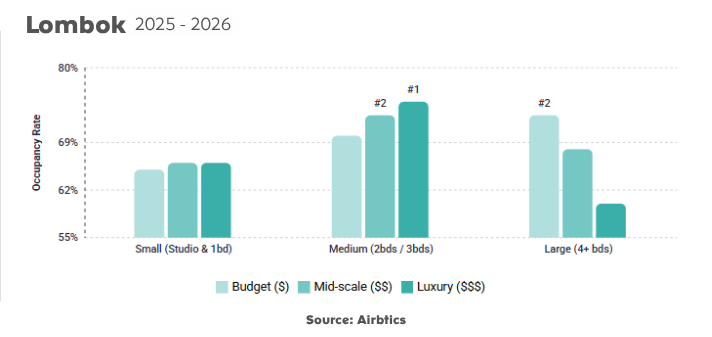

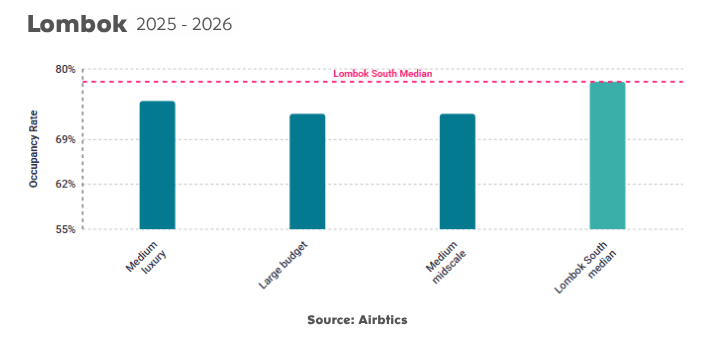

The most critical insight for a developer looking at Lombok is the sheer dominance of the Medium (2 to 3 bedroom) asset class. This size category dramatically outperforms both the smaller studios and the sprawling mega-villas. Within this 2-3 bedroom segment, the Mid-scale and luxury tiers are the absolute market leaders, pushing occupancy rates up toward the 73-76% mark.

Why does this specific configuration works? Because it perfectly aligns with the demographic. A 2-3 bedroom luxury villa caters to the affluent remote-working couple who requires a dedicated home office, or two couples splitting a premium asset for a two-week surf trip.

Conversely, the data serves as a stark warning against overbuilding. Look closely at the Large (4+ beds) category. While budget and mid-scale large villas perform adequately, the Luxury ($$$(USD)) 4+ bedroom segment plummets to roughly 60% occupancy.

The investment logic here is clear: Lombok does not yet possess the critical mass of ultra-high-end dining, beach clubs, and VIP infrastructure required to consistently attract massive groups of ultra-wealthy travelers. If you build a sprawling, 5-bedroom super-villa in Kuta-Lombok today, you will struggle to fill it at a premium rate because the surrounding neighborhood infrastructure does not yet support that level of group consumption. In Lombok, capital efficiency means capping your builds at 3 bedrooms and focusing heavily on high-end interior finishes.

Furthermore, the budget analysis confirms that the "Lombok median" performs exceptionally well, with "Medium luxury" tightly following. Investors should avoid racing to the bottom with budget builds; the market is actively rewarding quality, provided the bedroom count remains sensible.

The Gili Islands

If Lombok is about the couple and the digital nomad, the Gili Islands are entirely about the group. Gili Trawangan, Meno, and Air are destination micro-ecosystems. Travelers do not go there to work on their laptops for a month; they go for short, intense bursts of vacationing, diving, and celebrating with friends and family.

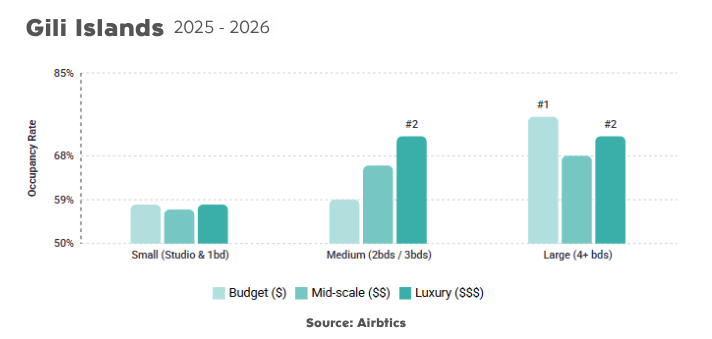

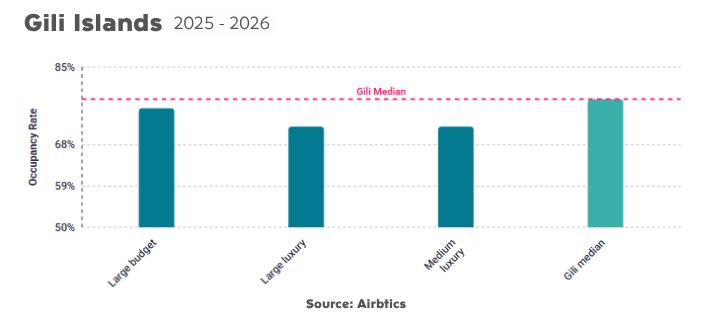

This demographic reality completely inverts the architectural logic of the mainland. In the Gili Islands, the Large (4+ beds) category is the undisputed champion of occupancy. Specifically, the Budget ($) and Mid-scale ($$) large villas absolutely dominate the market, pushing into the mid-70% occupancy range, with Large Luxury closely behind at roughly 70%.

When a group of six friends or two families travels via fast boat from Bali to the Gilis, they want to consolidate into a single, private compound. They want the shared pool, the communal living space, and the exclusive island vibe.

Conversely, the Small (Studio & 1bd) category across all budget tiers performs poorly, languishing in the sub-60% range. Solo travelers and couples visiting the Gilis on a budget typically opt for traditional homestays or boutique hotel rooms rather than renting a standalone 1-bedroom villa. Therefore, building a 1-bedroom investment property in the Gilis is an inefficient use of highly expensive, logistically challenging island real estate.

The budget breakdown further reinforces this. The "Large budget" and "Gili median" properties command the highest occupancies. The strategy for the Gilis is volume and footprint: build larger properties that can accommodate groups, but keep the operational pricing competitive. The goal is to capture the friends' trip or the wedding party, providing a premium communal experience without over-indexing on ultra-luxury fixtures that are incredibly difficult to maintain in a harsh, salty, car-free environment.

Managing the Seasonality

Regardless of whether you build a 3-bedroom luxury unit in Lombok or a 5-bedroom group compound in the Gilis, an investor must be prepared for the realities of regional seasonality. This is the "tax" of investing outside of Bali's year-round baseline.

Looking back at the primary revenue charts for both regions, the seasonality curves are extreme. Both Lombok and the Gili Islands experience a massive, vertical surge during the July and August high season, pushing occupancy to virtually 100%. During these months, the islands are at maximum capacity, and nightly rates can be pushed to their absolute limits.

However, the drop-off is equally aggressive. By November, and again in January and February, occupancy in both regions plummets toward the 50-60% floor. Nightly rates contract significantly as operators slash prices to capture whatever residual demand exists during the rainy season.

For an asset manager or investor, this extreme elasticity dictates the entire financial strategy. You cannot project linear, month-over-month cash flow in these markets. An asset here must be designed to generate the lion's share of its annual revenue in a concentrated 4-to-5-month window. The remaining months are about capital preservation and covering operational overhead. Success in Lombok and the Gilis requires aggressive dynamic pricing system, proactive offseason marketing, and a property management team that knows how to pivot from high-turnover operations to long-stay, discounted tenant retention during the quiet months.

Capital Placement Proposition

If you are entering Lombok, you build for the affluent couple: 2-to-3 bedrooms, mid-to-luxury finishes, and high daily utility. If you are crossing to the Gilis, you build for the group: 4+ bedrooms, communal layouts, and durable, competitive pricing.

Yield is about matching the exact structural asset to the behavioral psychology of the guest. The demand is already there, waiting at 78% occupancy. The investors who understand the sizing and the seasonality will be the ones who capture it.