Southeast Asia has never had a shortage of places that look remarkably good on paper. Warm weather, a low cost of living, rapidly growing expatriate communities, and the tantalizing promise of passive rental income form a familiar baseline. The investment pitch sounds almost identical whether you are looking at a beachfront villa in Phuket, a modern condominium in Langkawi, or a hillside property in Cebu.

But when you move past the initial lifestyle appeal and closely examine what the real estate numbers actually show, it becomes clear that these regional markets are not created equal. For expats, property investors, and digital nomads thinking seriously about allocating capital to property in the region, the data points consistently and undeniably in one direction.

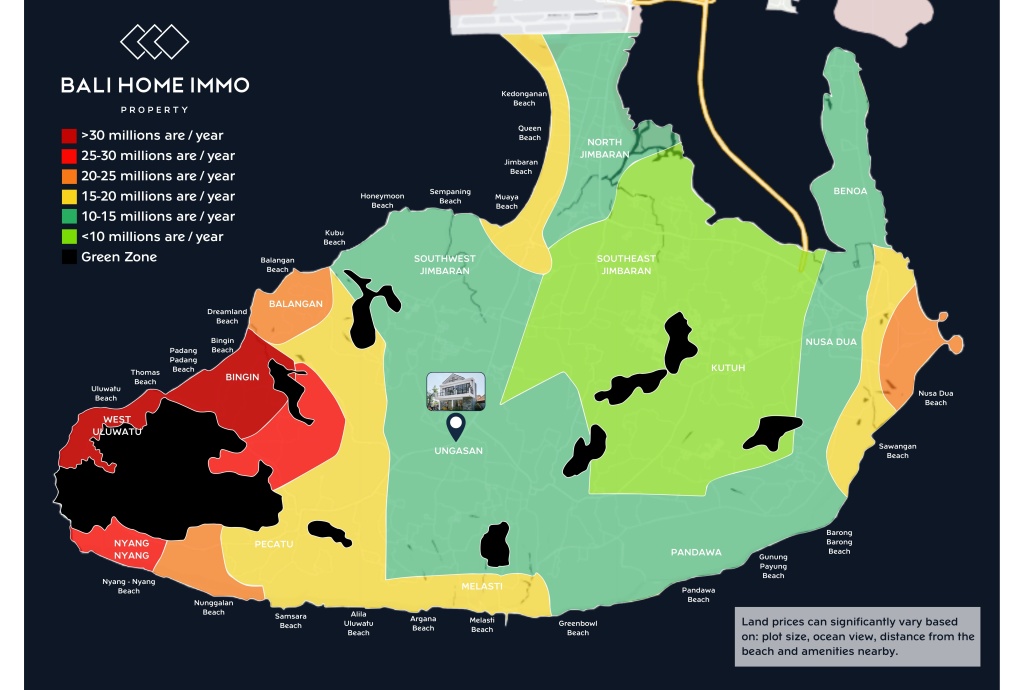

What the Daily Market Data Actually Shows

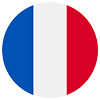

Short-term rental (STR) performance stands as one of the clearest, most transparent indicators of a property market's underlying investment health. It directly reflects real demand from real guests, priced dynamically by the market, and tracked meticulously over time. When you compare standalone beachfront villa performance across four of Southeast Asia's most talked-about expatriate destinations, Bali, Phuket, Langkawi, and Cebu, the performance gaps are significant.

The data presented below reflects regional market averages for each destination, not the performance of individual villas. Furthermore, this dataset is mined exclusively from premium beachfront properties.

Understanding the Monthly Curves

Annual revenue totals only tell part of the investment story. The shape of demand across the calendar year tells another. A highly seasonal market that yields one exceptionally strong quarter followed by nine weak ones creates severe cash flow bottlenecks for investors who need to service fixed operating costs year-round.

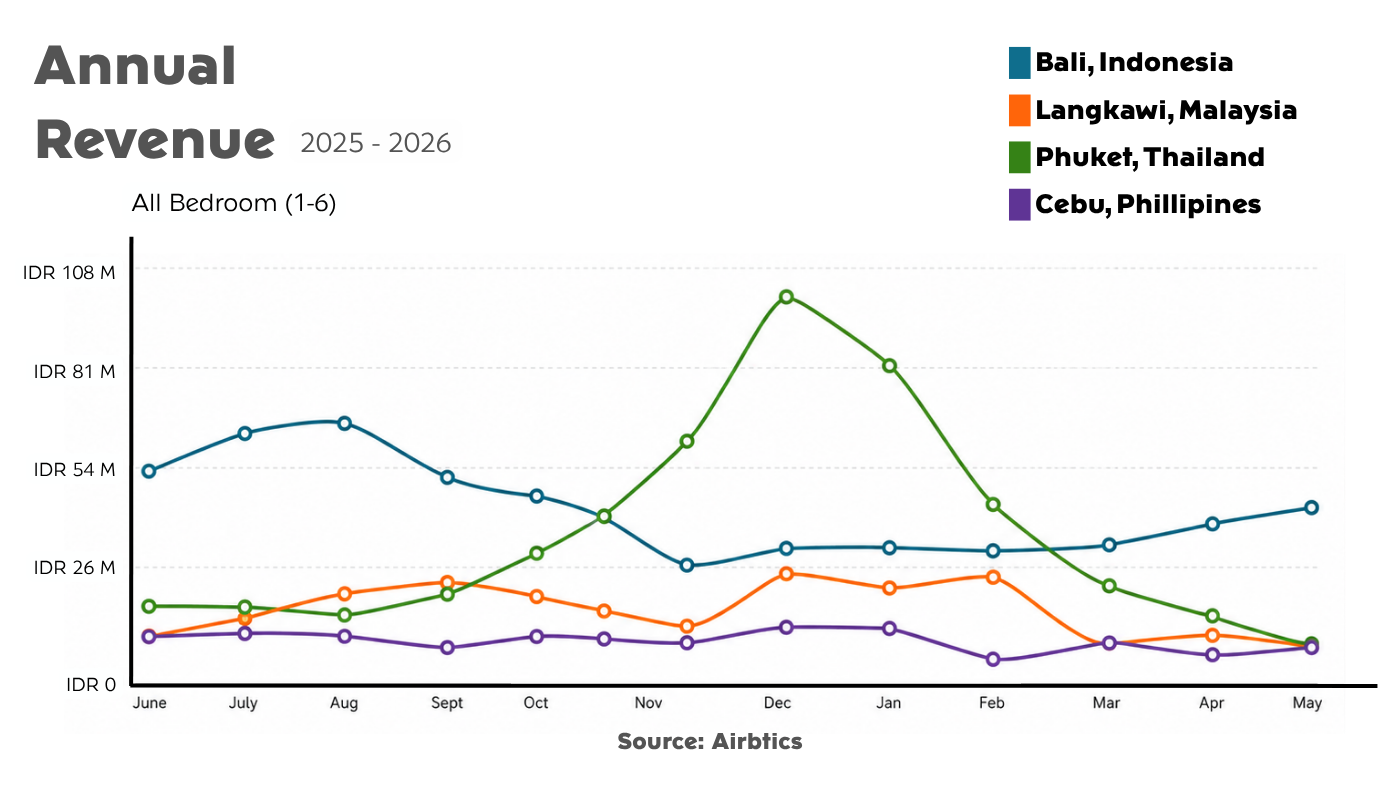

Bali’s median annual revenue sits at IDR 478.3M ($29,893), driven by a stable 64% occupancy rate and a premium nightly rate of IDR 2.0M ($126).

This curve shows a highly favorable distribution throughout the year. Monthly revenue peaks at approximately IDR 67M during July and August, softens through the November to March period where it settles around IDR 35M per month, and then recovers steadily from April onward. Importantly, even at the low season floor, monthly revenue does not drop below IDR 35M. That baseline predictability matters far more than temporary peaks when mapping out long-term investment planning.

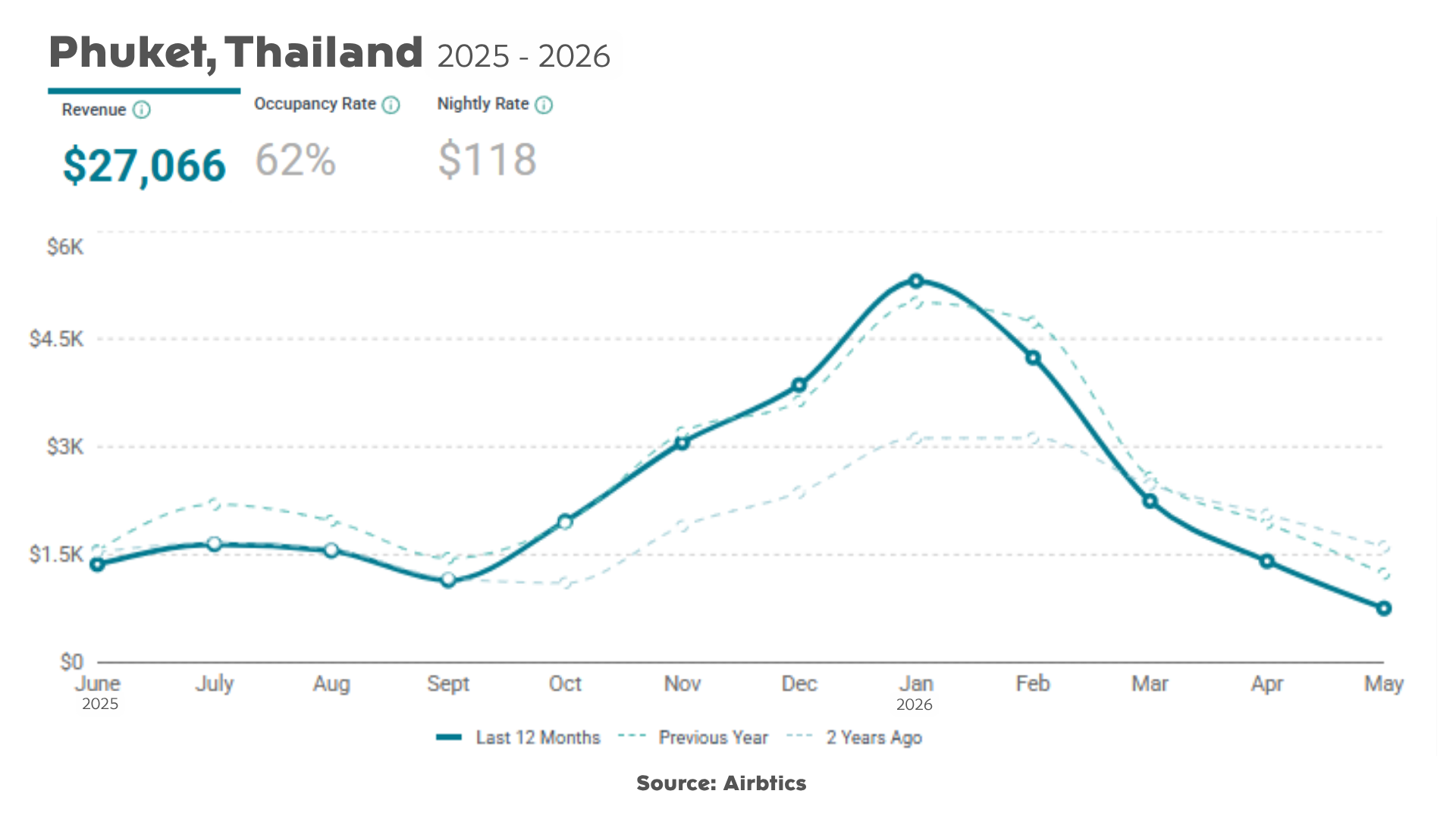

Phuket's Seasonal Swing Requires Active Management

Phuket shows a much more pronounced and dramatic seasonal swing. Monthly revenue opens at approximately IDR 26M in June, stays flat through September, then climbs sharply through November and December, peaking at close to IDR 99M in January before collapsing back toward IDR 10M by May.

As the closest regional competitor, Phuket posts IDR 433.1M ($27,066) in annual revenue, a 62% occupancy rate, and an IDR 1.9M ($118) nightly rate.

For property investors, this seasonal volatility means Phuket can produce strong headline annual numbers while requiring highly active management, dynamic pricing strategies, and careful cash flow reserves to maintain year-on-year performance. The gap between Phuket's January peak and its May trough is nearly IDR 90M, a swing that demands serious operational planning.

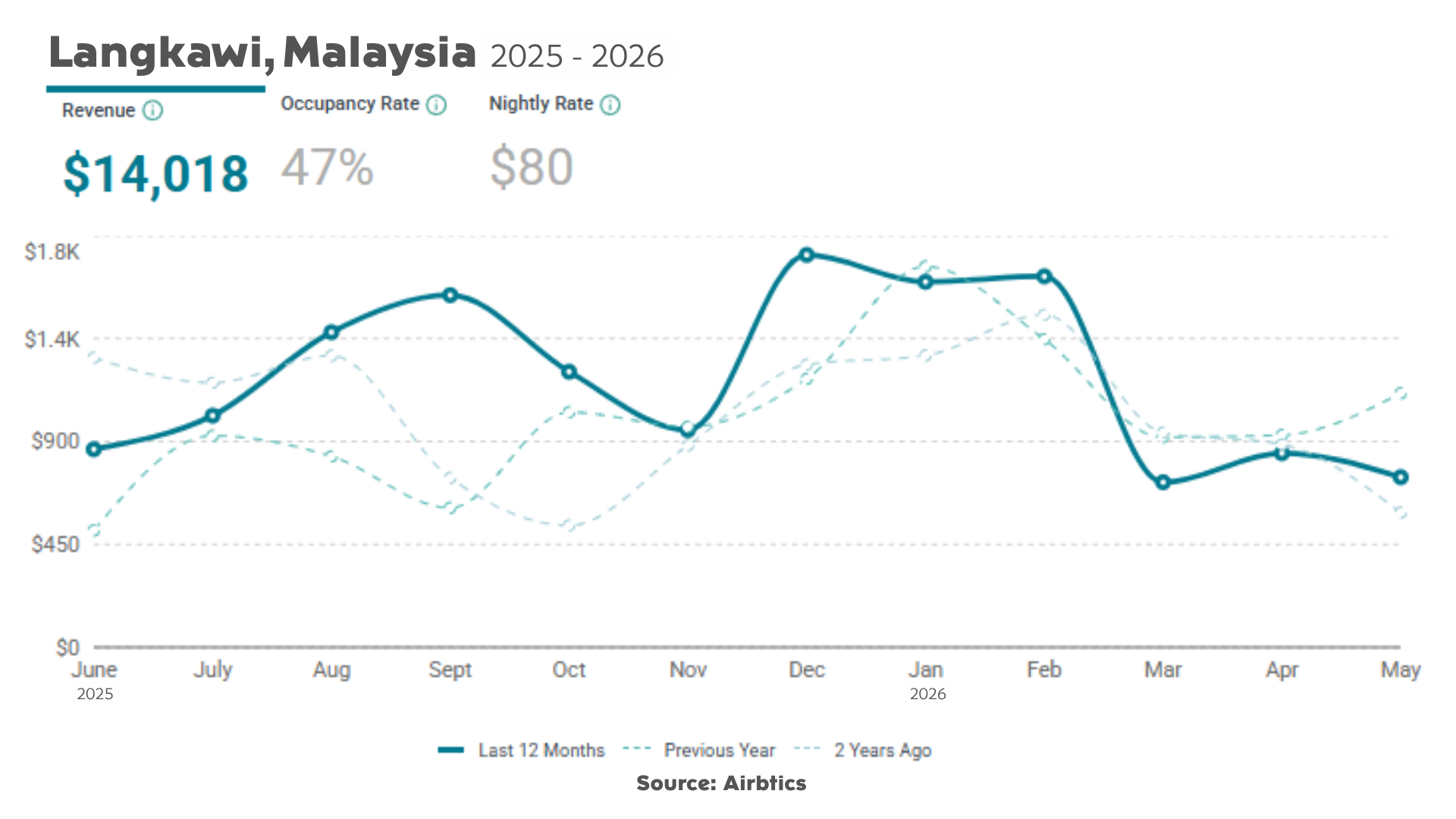

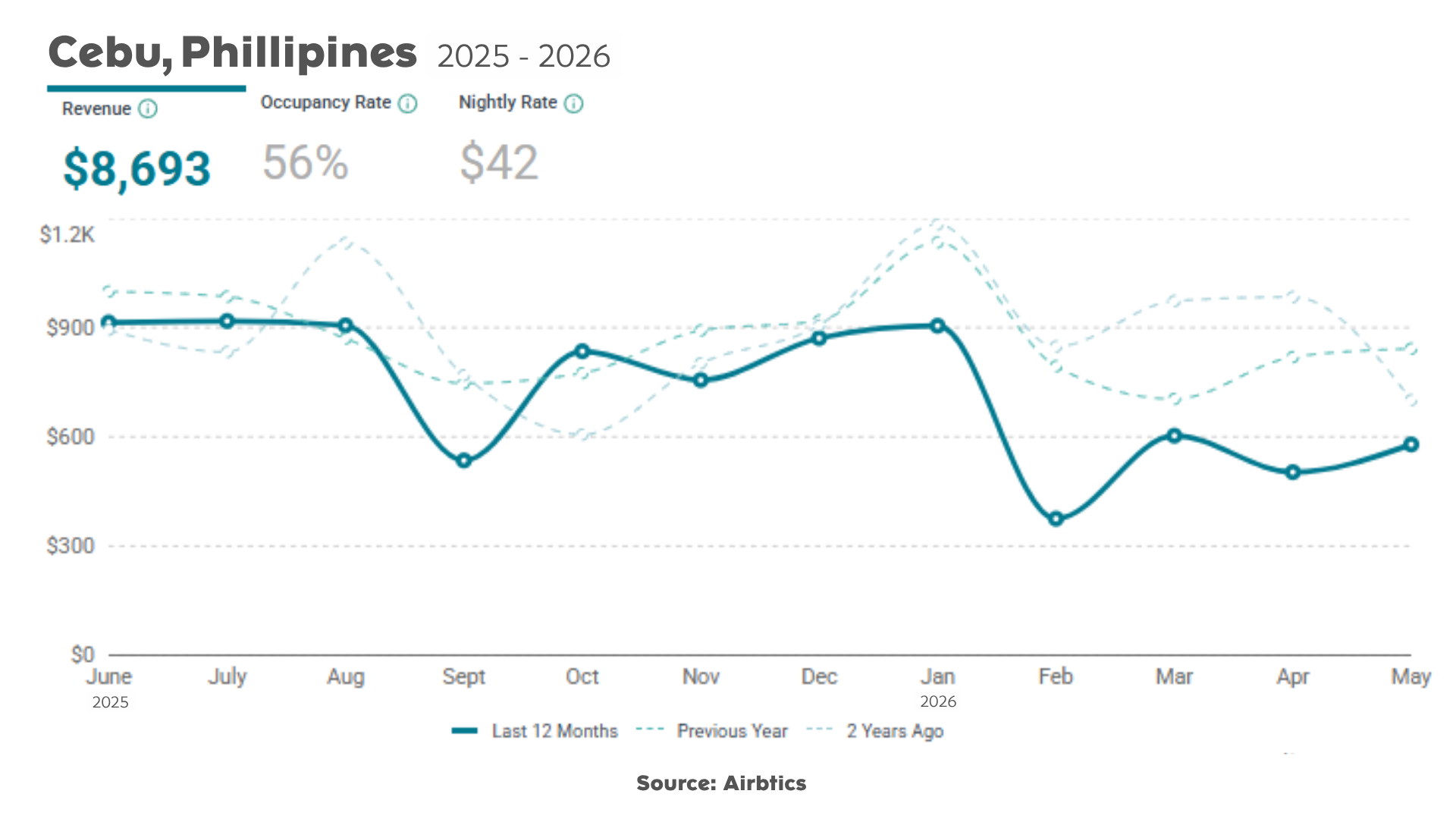

Langkawi, and Cebu: Early-Stage Profiles

This Malaysian destination shows IDR 224.3M ($14,018) in annual revenue at a 47% occupancy rate and an IDR 1.3M ($80) nightly rate.

Digging into the monthly trajectory, Langkawi presents a unique, multi-modal line profile characterized by two distinct mini-peaks. The first surge occurs in August and September, pushing monthly revenues up to approximately IDR 28M. The line then softens briefly before climbing to its secondary, dominant peak from December through February, reaching IDR 30M. The downside of this trendline occurs from March onward, where the curve drops sharply and flattens out at IDR 13M for the remainder of the spring and early summer. This double-cycle graph indicates a market dictated by specific, segmented regional holiday calendars rather than global, year-round migration waves.

Cebu's curve is flatter but more volatile, ranging mostly between IDR 13M and IDR 16M per month with notable dips in September to around IDR 10M and in February down to approximately IDR 6M.

These metrics clearly reflect a budget-conscious tourism market rather than an investment-grade real estate arena. Furthermore, Cebu’s monthly curve is structurally restricted by its nightly price caps. The trendline spends the majority of the year oscillating tightly between a narrow band of IDR 13M and IDR 16M per month. While it appears relatively flat on a macro scale, it exhibits highly erratic micro-volatility. The line suffers a sharp dip in September down to IDR 10M, encounters a brief year-end recovery, and then experiences a deep, sudden trough in February, dropping to an operational low of approximately IDR 6M. This behavior indicates a market driven by highly erratic weekend domestic tourism and volatile budget travelers, preventing operators from establishing a stable, premium pricing baseline.

Both markets primarily suit patient investors with a longer time horizon and lower near-term income expectations. Neither acts as a direct competitor to Bali for income-focused buyers today.

The Legal Dimension:

Brilliant yields mean very little if the underlying legal ownership structures expose your capital to unnecessary risk. Every country in Southeast Asia treats foreign property ownership differently.

Thailand: Condominiums Yes, Land No

In Thailand, foreigners are strictly prohibited from owning land outright in their personal name. Condominium ownership is legally available under the Thai Condominium Act, provided that total foreign ownership within a specific building does not exceed 49%. For villas and landed property, the exact asset classes that generate the strongest short-term rental returns, foreigners must typically rely on long-term leases or complex Thai company structures, both of which carry distinct legal, corporate, and practical limitations over time.

Malaysia and the Philippines: Partial Access

Malaysia permits foreign property ownership but enforces strict minimum price thresholds that vary significantly by state to protect local buyers. While the MM2H (Malaysia My Second Home) program has historically offered a reliable residency pathway, the entry barriers remain high. The Philippines allows foreigners to fully own condominium units, but land ownership is legally barred. In both nations, the most lucrative short-term rental asset class, standalone holiday villas, is either heavily restricted or structurally complex to hold securely as a foreign national.

Bali: Established Pathways with a Long Track Record

Foreigners cannot hold Hak Milik (freehold land title) in Indonesia, but there are legitimate, well-established structures for international investment:

-

Leasehold (Hak Sewa): Typically structured over an initial 25 to 30 years, backed by legally binding extension options written directly into the contract.

-

Right-to-Use (Hak Pakai): A title registered directly with the land office, available to individual foreigners who hold a valid Indonesian residency permit.

-

PT PMA: A foreign-owned Indonesian limited liability company that allows institutional investors to conduct commercial hospitality operations and hold direct corporate control over real estate assets.

What Bali offers that smaller regional markets cannot match is a deeply mature legal ecosystem. The island handles high transaction volumes supported by a well-developed notary and legal services industry, with years of clear precedent for foreign investment. Working with a licensed agency and an independent notary remains essential, but the framework is fully established and transparently navigable.

Truth to be told..

When the objective is strictly maximizing Return on Investment (ROI), the data across Southeast Asia leaves no room for debate: Bali is the single most profitable real estate market in the region. While emerging locations might tempt buyers with lower initial entry prices, they fundamentally lack the infrastructure, year-round demand, and premium nightly rates required to generate elite, consistent cash flow.

Bali’s unique dual-market ecosystem, capturing both high-spending short-term vacationers and a massive, year-round expatriate community, creates an elevated revenue floor that other regional markets simply cannot replicate. For serious foreign investors looking to acquire a mature, high-yielding, and rapidly compounding asset, Bali stands alone as the ultimate, highest-ROI investment destination.